The Pension Theft: How Boomers Sold Their Children's Future

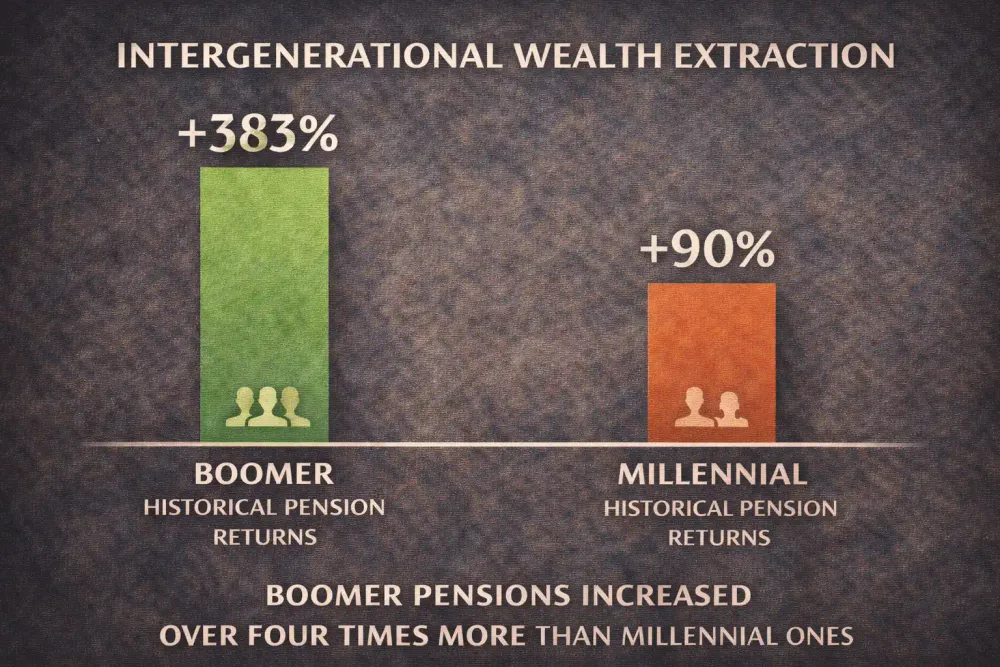

Italy spends 16.2% of GDP on pensions, more than education, defense, and infrastructure combined. Average French boomer paid in €180,000, receives €685,000 (383% return). French Millennial pays in €360,000, receives €180,000 if lucky (90% return = 10% loss).

Italy spends 16.2% of GDP on pensions - highest in the developed world, mathematically unsustainable.

Average French boomer: paid in €180,000, will take out €685,000 - a 380% return their children will never see.

Greek pension age: 67 - but average retirement age is 61.5 through disability and early retirement loopholes.

Millennials will receive 30-50% less in pension value than they pay in - if the systems survive at all.

€2.1 trillion in unfunded pension liabilities across the EU - debt pushed onto future generations who can't vote yet.

Introduction

There's a theft happening across Europe right now. Not a robbery, those are quick, violent, obvious. This is slow, systematic, and sanctioned by law. It's the largest wealth transfer in European history, and it's flowing in one direction: from young to old, from workers to retirees, from Millennials to Baby Boomers.

The mechanism is pension systems that were sold as intergenerational compacts but function as Ponzi schemes. The beneficiaries are retirees who paid in a fraction of what they're taking out. The victims are workers in their 20s, 30s, and 40s who are funding retirements they'll never receive.

This isn't speculation. It's mathematics. And the numbers are fucking terrifying.

Italy spends more on pensions than on education, defense, and infrastructure combined. France nearly collapsed in 2023 over raising the retirement age from 62 to 64, two years. Spain's pension reserve fund, built to protect the system, has been 96% depleted in just over a decade. Germany faces a demographic time bomb that will require either 40%+ pension taxes or slashing benefits in half.

The European pension crisis isn't coming. It's here. And it's not a crisis of demographics or economics, it's a crisis of political will. Boomers voted themselves generous benefits they refused to fund, expanded entitlements as they approached retirement, and now block any reform that would make the systems sustainable.

The generational compact was simple: you pay for your parents' retirement, your children pay for yours. Boomers broke it. They paid in at lower rates, for fewer years, during economic boom times. They're taking out at higher rates, for longer periods, during demographic collapse. And they're leaving their children with nothing but debt, broken promises, and a political system captured by retiree interests.

This investigation exposes how pension systems became extraction machines, which countries are the worst offenders, who profits from the scam, and why reform is politically impossible. It documents the mathematical impossibility of maintaining current promises, the generational theft mechanics that transferred trillions from young to old, and the coming collapse that will impoverish both generations.

The evidence is in government data, demographic projections, and simple arithmetic. The conclusion is inescapable: the European pension system is the largest intergenerational fraud in history.

And it's your future being stolen.

By A. Kade

What This Investigation Exposes

The mathematical impossibility of European pension systems and how demographic collapse meets benefit expansion to guarantee bankruptcy. The Boomer generation's extraction of 300-400% returns on pension contributions while Millennials face 30-50% losses. Country-by-country devastation across Italy, France, Greece, Spain, and Germany showing how each system is failing. The political capture that makes reform impossible when pensioners vote at 75% and youth at 35%. The private pension scam where fees consume 30-40% of returns while workers pay twice, publicly for boomers, privately for themselves. The austerity hypocrisy that cuts youth programs while protecting pensions. The asset hoarding that locks Millennials out of housing while boomers sit on accumulated wealth. The three scenarios for collapse and why all end with generational theft. The reforms that would work and why boomers block them. And the moral obscenity of a generation that benefited from unprecedented prosperity telling their impoverished children they're lazy.

The truth doesn’t trend. It survives because a few still care enough to keep it alive.

Keep The Kade Frequency transmitting.

The Mathematical Impossibility

European pension systems are Ponzi schemes that worked for exactly one generation: the Boomers. The scheme required a specific set of conditions that no longer exist and will never return.

In 1970, there were five workers supporting each pensioner, a ratio of 5:1 that made the pay-as-you-go model sustainable. Workers paid modest contributions (10-15% of salary), pensioners received modest benefits (40-50% of final wage), and the math worked. As long as you had five people paying in for every person taking out, the system balanced.

By 2024, that ratio has collapsed to 2.5 workers per pensioner. According to Eurostat population projections, by 2050 it will be 1.5:1. The OECD Pensions Database shows this isn't a temporary dip, it's the new permanent reality of Europe's demographic structure.

But here's where the Ponzi scheme becomes obvious: while the worker-to-pensioner ratio was collapsing, benefits were expanding. Pension payments increased 40% in real terms from 1970 to 2024. Retirement ages dropped (France from 65 to 62, Italy introduced early retirement at 57). Life expectancy increased by 15 years, meaning 20-30 years in retirement instead of 5-10.

So fewer workers are supporting more pensioners for longer periods at higher benefit levels. This violates basic arithmetic. You cannot have:

- Fewer contributors (2.5 vs 5 workers per pensioner)

- More beneficiaries (aging population)

- Higher benefits (40% increase)

- Longer payment periods (20-30 years vs 5-10)

And expect the system to survive.

The European Commission's Ageing Report projects pension expenditures rising from 11.2% of GDP in 2020 to 13.9% by 2050 under current policies. That's an additional 2.7% of GDP, roughly €400 billion annually, that has to come from somewhere. Either taxes rise dramatically, benefits get cut massively, or the system collapses.

The Boomers hit the perfect timing window. They entered the workforce during the golden age of capitalism (1960s-1980s) when the ratio was 5:1 and benefits were being expanded. They paid in during boom times with high wage growth and low dependency ratios. They're retiring now, extracting benefits funded by a shrinking workforce in stagnant economies.

And that window has closed permanently.

The Boomer Extraction

Let's run the numbers on what Boomers paid in versus what they're taking out. This is where the theft becomes undeniable.

What Boomers Contributed:

A French boomer born in 1950, entering the workforce in 1975, retiring in 2020:

- Worked 45 years (1975-2020)

- Paid pension contributions averaging 10-12% of salary

- Average real wages doubled during their career (1975-2020 wage growth)

- Total contributions: approximately €180,000 (inflation-adjusted)

What Boomers Receive:

That same French retiree:

- Retirement at age 62 (before recent reform to 64)

- Life expectancy: 85 years = 23 years in retirement

- Average pension: €30,000 per year

- Total received: €30,000 × 23 years = €690,000

The Return:

€690,000 received ÷ €180,000 contributed = 383% return on investment

Show me a private investment that guarantees 383% returns over 45 years with zero risk. It doesn't exist. This "return" isn't from investment growth, it's extracted from current workers.

Compare that to a Millennial's math:

What Millennials Pay:

A French Millennial born in 1990, entering workforce in 2015, retiring in 2060:

- Will work 45 years (2015-2060)

- Paying pension contributions of 24-28% of salary (more than double Boomer rates)

- Stagnant real wages (flat since 2000)

- Total contributions: approximately €360,000 (double what Boomers paid)

What Millennials Will Receive:

Under current demographic projections:

- Retirement at age 70 (if not raised further)

- Life expectancy: 88 years = 18 years in retirement

- Projected pension: €18,000 per year (30-40% cut from promised levels)

- Total received: €18,000 × 18 years = €324,000

The Return:

€324,000 received ÷ €360,000 contributed = 90% return

That's not a return, that's a 10% loss. After paying in twice as much as Boomers, Millennials will receive half as much. If the system survives at all.

The IMF Fiscal Monitor calculations show unfunded pension liabilities across the EU exceeding €2.1 trillion. That's the gap between what's been promised and what can be paid. Someone has to cover that gap. It won't be the Boomers, they're already retired. It will be Millennials, through higher taxes, later retirement, and benefit cuts.

This is the extraction mechanism: Boomers voted for benefit expansions during their working years (1970s-1990s), knowing they'd be the beneficiaries. They voted against funding increases that would have made those benefits sustainable. They kicked the bill down the road to their children.

Now those children are discovering the bill: €360,000 paid in, €324,000 received out, if they're lucky. More likely: €150,000-€200,000 received if the system is "reformed" (code for: cuts). Possibly nothing if it collapses entirely.

The average Boomer extracted €510,000 more than they contributed (€690,000 - €180,000). That money came from somewhere. It came from Millennials paying 24-28% of their salary into a system that will give them nothing close to equivalent value.

That's not a pension system. That's a fucking heist.

"A society grows great when old men plant trees in whose shade they shall never sit." - Greek Proverb

The Boomers didn't plant trees. They cut them down, sold the lumber, and told their children to plant their own.

Italy: The Pension State

Italy is ground zero for the European pension catastrophe. It's the extreme case, the cautionary tale, the place where the math became impossible first.

Italy spends 16.2% of GDP on pensions. To put that in perspective: the OECD average is 8-9%. Italy spends more on pensions than it spends on education, defense, and infrastructure combined. The entire country functions to extract wealth from workers and transfer it to retirees.

This isn't because Italians are particularly generous. It's because the system was captured by retiree interests and expanded to the point of absurdity.

The Baby Pensioner Scandal:

Italy has thousands of "baby pensioners", people who retired in their 40s and 50s with full benefits and have been collecting for 30-40 years. This wasn't a bug, it was policy.

In the 1980s and 1990s, Italy introduced seniority pensions: retire after 35 years of contributions regardless of age. If you started working at 18, you could retire at 53. Public sector workers got even better terms: 30 years for women, 35 for men, retire in your late 40s.

The result: people retiring at 48-52 years old, collecting pensions for 35-40 years, receiving more in retirement than they earned working. One investigation found a teacher who retired at 47 and collected a pension for 41 years, receiving benefits for nearly as long as she worked.

This system "reformed" in 1995, then 2011, then 2019. Each reform was supposed to fix the crisis. None did, because the political cost of real reform is electoral suicide.

The Special Regimes:

Italy maintains dozens of special pension regimes for politically connected groups:

- Postal workers: retire at 57

- Public sector employees: retire at 60 (vs 67 for private sector)

- Miners and quarry workers: retire at 50 (because "arduous", never mind modern equipment)

- Flight attendants: retire at 55 (because flying is "stressful")

These special regimes are protected by unions, political parties, and voting blocs. Attempts to equalize them trigger strikes and political crises.

The Disability Pension Epidemic:

In parts of Southern Italy, disability pensions are a cultural institution. One investigation in Sicily found a town of 4,000 residents with 1,000 people on disability pensions, 25% of the population suddenly "disabled."

Further investigation revealed 80%+ were fraudulent. The scam: doctors would certify anyone as disabled for a fee, relatives would claim disability for dead family members, entire families would go on disability together. The government knows it's happening but can't stop it, the Mafia enforces the system and politicians need the votes.

The result: billions spent on fake disability payments while youth unemployment in Southern Italy hits 40-50%.

The Youth Sacrifice:

Italy's youth unemployment rate: 23.7% nationally, 40-50% in the South. Meanwhile pension spending is protected absolutely. During the austerity years (2010-2015), Italy cut:

- Education spending: -15% per student

- Youth employment programs: -40%

- University funding: -20%

- Infrastructure investment: -25%

Pensions? Cut 3%. And that 3% cut triggered protests and political instability.

The message to Italian youth: we will impoverish you, destroy your employment prospects, gut your education, and demand you fund retirements we'll never provide you. Then we'll call you lazy for emigrating.

Over 500,000 Italians aged 20-35 have left Italy since 2010. They're not leaving because of avocado toast. They're leaving because the country has been optimized to extract wealth from workers and give it to retirees, and they're the workers being extracted from.

The Impossible Math:

Italy's worker-to-pensioner ratio: 1.8:1 (and falling). To maintain current pension promises would require:

- Raising pension contributions to 40-45% of wages, or

- Raising the general tax rate by 15-20 percentage points, or

- Cutting all other government spending by 50%

None of these is politically or economically possible. So Italy lurches from crisis to crisis, making token reforms that don't fix the math, while the debt grows and youth emigrate.

The European Commission warned Italy in 2019 that its pension system is "not sustainable." Italy's response: promise to reform eventually while changing nothing.

Millennials are watching their contributions disappear into a system that will give them nothing, while being told they're entitled for questioning it.

France: The Untouchable Retirement

France is where the political impossibility of pension reform became undeniable. It's where a government nearly collapsed over raising the retirement age by two years. Two. Fucking. Years.

The 2023 Reform Battle:

President Emmanuel Macron proposed raising France's retirement age from 62 to 64. Not 70. Not 65. 64. Still the lowest in the developed world except Turkey.

The response: months of riots, millions in the streets, garbage piling up as workers struck, government stability threatened. Macron eventually forced it through using a constitutional mechanism that bypassed a vote, essentially a legal coup to implement a tiny reform.

Why? Because French retirees and public sector workers have captured the political system so completely that even modest reforms trigger revolution.

The Special Regimes:

France maintains pension regimes so absurd they read like satire:

Train drivers (SNCF): Retire at 52 with 75% of final salary as pension. Yes, 52. The justification: "arduous work conditions." These are people sitting in air-conditioned cabs pushing buttons.

Electricity workers (EDF): Retire at 55. They literally supply the power that runs the country, have stable employment, good pay, and retire at 55 while everyone else works to 64.

Opera workers: Retire at 57. Singing is classified as arduous labor. Meanwhile construction workers, actual arduous labor, work to 64.

Paris Metro drivers: Retire at 50. Underground work is considered so hazardous that half a century is the maximum. Never mind office workers in basements or miners elsewhere who work full careers.

These special regimes cost billions. Reform attempts in 1995, 2003, 2010, and 2023 all triggered massive strikes and political crises. The regimes remain protected.

The Numbers:

France spends 14.7% of GDP on pensions, second only to Italy. The European Commission Ageing Report projects this rising to 16%+ by 2040 under current promises.

The Pensions Advisory Council (Conseil d'Orientation des Retraites) calculated that maintaining current pension levels would require:

- Raising the retirement age to 68-70, or

- Increasing pension contributions by 5-7 percentage points, or

- Accepting deficits of €50-€80 billion annually

France chose option four: deny the problem exists and hope it goes away.

The Boomer Return:

Average French boomer (as calculated earlier):

- Paid in: €180,000

- Takes out: €685,000

- Return: 383%

Average French Millennial (projected):

- Paying in: €360,000

- Will receive: €200,000-€250,000 (if system "reformed")

- Return: 55-70% (a loss, not a return)

The Political Capture:

Why is reform impossible? Voter demographics:

- Over-65s: 25% of registered voters, 75% turnout = 28% of actual votes

- Under-35s: 20% of registered voters, 35% turnout = 10% of actual votes

Any politician proposing real reform loses 28% of votes instantly. Young people whose futures are being stolen don't vote enough to matter. So politicians pander to retirees.

The result: France is heading toward pension bankruptcy while being politically incapable of preventing it.

Macron got his two-year increase. It took months of riots and constitutional maneuvering. That's what a tiny reform costs. Real reform, retirement at 70, benefit cuts, special regime elimination, would trigger civil war.

So the can gets kicked, and Millennials get billed.

Greece: The System That Already Collapsed

Greece is Europe's pension future: the place where the math caught up, the system collapsed, and everyone got poorer. It's a preview of what happens when you maintain the unsustainable until it becomes impossible.

Before the Collapse:

Pre-2010 Greece had pension generosity that made France look austere:

- Average retirement age: 58 (official 65, but loopholes everywhere)

- Pension payments: 14 months per year (monthly pension × 14, not 12)

- Christmas bonus: extra month's pension

- Easter bonus: extra month's pension

- Summer bonus: extra half-month

- Average pension: 95% of final salary for public sector

- "Arduous professions": 580 job categories classified as arduous (including hairdressers)

The hairdresser thing isn't a joke. Greek hairdressers could retire at 50 with full pensions because cutting hair was deemed arduous labor. Also classified as arduous: musicians, radio announcers, and people who worked with "noxious substances" (defined broadly enough to include perfume counter workers).

The system was pure fantasy. Greece had 2.6 million pensioners and 4.5 million workers, a ratio of 1.7:1. Each worker supporting 0.6 pensioners, while also paying for government services, and doing so in an economy with massive tax evasion.

The math was impossible. Everyone knew it. Nobody fixed it because fixing it meant electoral defeat.

The Collapse:

The 2010-2015 debt crisis forced Greece into EU/IMF bailout programs. The bailouts came with conditions: pension reform or no money. Greece had no choice, it was bankrupt.

The "reforms":

- Pensions cut 40-50% (not reduced, cut from existing pensioners)

- Retirement age raised to 67

- 14-payment system reduced to 12

- Special regimes mostly eliminated

- Eligibility tightened

The result: pensioners who'd paid in for 30-40 years saw their income halved. Some literally couldn't afford food or medicine. The suicide rate among elderly Greeks increased 35%.

This was real reform, the kind that actually addresses the math. And it was catastrophic for those who'd relied on the promises.

The Lesson:

Greece shows what happens when you delay reform until crisis forces it. If Greece had reformed gradually in the 1990s, raising retirement age incrementally, reducing benefits slowly, eliminating special regimes over time, the pain would have been distributed and manageable.

Instead they delayed until the system collapsed. Then the IMF and EU forced brutal cuts overnight. Pensioners lost half their income with no warning and no time to adjust.

This is the future for Italy, France, Spain, and others that refuse to reform: delay until crisis, then brutal cuts imposed by creditors or demographic reality.

The Continuing Dysfunction:

Even after "reform," Greece still spends 13.9% of GDP on pensions. The system is still unsustainable. The cuts were enough to stabilize temporarily but not enough to fix the long-term math.

Greek Millennials are paying into a system that collapsed once and will collapse again. They have zero faith in receiving benefits. Many don't bother checking their pension statements, there's no point. The money they're forced to contribute is just another tax, not a retirement investment.

The Greek pension system is a cautionary tale in slow motion: how political cowardice turns a solvable problem into a catastrophe.

"The sins of the fathers are to be laid upon the children." - William Shakespeare, The Merchant of Venice

The consumption of the fathers is billed to the children. With interest.

Spain: The Reserve Fund Raid

Spain built a pension reserve fund during the boom years, a €67 billion cushion to protect the system during demographic stress. It was supposed to be untouchable, invested wisely, growing to support future retirees.

In 2024, there's €2 billion left. They spent 96% in just over a decade.

The Reserve Fund Scam:

Spain's pension reserve fund was established in 2000 when the economy was booming and pension contributions exceeded payouts. The surplus was supposed to be saved and invested, building a buffer for when demographics worsened.

By 2011, the fund peaked at €67 billion, roughly 6.5% of GDP. Spanish politicians congratulated themselves on fiscal responsibility and long-term planning.

Then they raided it.

Starting in 2012, as Spain's economy crashed and unemployment soared, pension contributions fell but payments continued. Rather than reform the system, the government simply withdrew from the reserve fund to cover the gap.

€5 billion in 2012. €7 billion in 2013. €11 billion in 2014. Every year, billions withdrawn to cover the shortfall between contributions and payments.

By 2024: €2 billion remains. The fund will be completely empty by 2025.

The Math They Ignored:

Spain's demographics are catastrophic:

- 10 million pensioners (and growing)

- 20 million workers (and shrinking)

- Ratio: 2:1 (and worsening rapidly)

- Birth rate: 1.2 children per woman (well below replacement)

- Youth unemployment: 28% (those who should be contributing, aren't)

The reserve fund was meant to cushion this demographic transition. Instead, it was spent maintaining unsustainable benefit levels to avoid political costs.

The Coming Crisis:

With the reserve fund depleted, Spain faces immediate choices:

- Cut pensions by 20-30% (politically impossible)

- Raise contributions by 8-10 percentage points (economically impossible)

- Borrow to cover the gap (adding to already high debt)

- Inflate away the obligations (destroying everyone's wealth)

Spain is choosing option three: borrow. Public debt is rising to cover pension payments. This pushes the cost onto future taxpayers, Millennials and Gen Z who will inherit massive debts from funding Boomer retirements.

The Generational Obscenity:

Spanish pensioner average income: €1,200/month Spanish youth (under 30) average salary: €1,100/month

Read that again: pensioners who aren't working earn more than young people who are. This is unprecedented. In a functioning economy, workers earn more than retirees. In Spain, the extraction has reversed the natural order.

Spanish youth respond by leaving. Over 500,000 emigrated in the past decade, the educated, the skilled, the mobile. They're leaving a system that taxes them at 30%+ to fund pensions they'll never receive, in an economy where pensioners earn more than workers.

The reserve fund raid is particularly galling because it was preventable. If Spain had reformed when the fund was built, gradually raising retirement age, moderating benefit increases, tightening eligibility, the fund could have lasted and eased the transition.

Instead: spend the cushion to avoid tough choices, leaving nothing for the crisis everyone knew was coming.

Millennials are watching in real-time as their pension contributions disappear into a system that burned through €67 billion in reserve and will have nothing left when they retire.

Germany: The Demographic Time Bomb

Germany faces the worst demographic crisis in Europe. Worse than Italy's pension spending, worse than France's political paralysis, worse than Spain's depleted reserves. Germany has the oldest population in Europe after Japan and a birth rate of 1.5, catastrophically below replacement.

The Numbers:

- Birth rate: 1.5 (need 2.1 for replacement)

- Over-65 population: 22% (and accelerating)

- Worker-to-pensioner ratio: 2.1:1 (falling to 1.3:1 by 2050)

- Pension expenditure: 10.1% of GDP (projected 12.5% by 2050)

The OECD Pensions Database shows Germany's problem isn't current spending, it's the accelerating collapse of worker ratios as Boomers retire and birth rates stay low.

The Political Commitment:

German law mandates pension levels at minimum 48% of average wages. This is legally binding. The retirement age was raised to 67 (one of the few countries to do so), but benefit levels are protected by law.

Maintaining that 48% as demographics worsen requires either:

- Increasing pension contributions from 18.6% to 25-30% by 2040, or

- Cutting benefits by 30-40% (requires changing the law), or

- Raising retirement age to 70+ (politically toxic)

Germany is paralyzed between economic reality and legal commitments.

The Riester Pension Scam:

Facing the demographic crisis, Germany introduced Riester pensions in 2002, subsidized private retirement accounts to supplement the state system. The pitch: the state pension won't be enough, save privately with tax advantages.

The reality: Riester pensions are a fee-extraction racket:

- Management fees: 1.5-2% annually

- Sales commissions: 4% upfront

- Administrative fees: €30-€60 per year

- Total cost: 35-40% of returns eaten by fees over 40 years

A Millennial contributing €100/month for 40 years:

- Total contributions: €48,000

- Expected value at 5% returns: €150,000

- Actual value after fees: €95,000

- Fees extracted: €55,000 (37% of returns)

The financial industry profits, workers get robbed, and politicians claim they've "solved" the pension crisis.

The Impossible Choice:

German Millennials are told:

- Pay 18.6% of salary into state pension (for Boomer benefits)

- Save 10-15% privately in Riester (for your own retirement)

- Total retirement savings: 28-33% of income

Meanwhile:

- Rent: 35-45% of income in major cities

- Student loans: €300-€500/month

- Health insurance: 15% of income

- Other taxes: 25-30% effective rate

The math is impossible. You cannot pay 33% for retirement + 35% for housing + 15% for health + 30% in taxes on Millennial wages.

The result: German Millennials are saving nothing for retirement while funding Boomer pensions they won't receive.

The Migrant "Solution":

German politicians propose immigration as the solution, bring in workers to improve the ratio. Some problems:

- You'd need 15-20 million immigrants to restore 1970s ratios (politically and socially impossible)

- Immigrants age too, they become pensioners eventually

- Integration costs billions (negating short-term fiscal benefits)

- German voters oppose mass immigration (AfD rise)

- Skilled immigrants go to Anglosphere countries with higher wages

Immigration might slow the decline but can't reverse it. The math still doesn't work.

The Coming Reckoning:

Germany will face its crisis in the 2030s as Boomers fully retire. The choices then:

- Break the 48% pension level law (political earthquake)

- Raise contributions to 30%+ (economic disaster)

- Borrow massively (debt crisis)

- Inflate obligations away (wealth destruction)

All options are catastrophic. Germany delayed reform for 30 years hoping for economic growth that didn't come. Now the bill is due.

The Political Impossibility of Reform

Here's why the pension crisis won't be fixed: pensioners vote, youth don't.

The Electoral Math:

Across the EU:

- Over-65s: 25-30% of registered voters

- Over-65 turnout: 70-80%

- Over-65 share of actual votes: 30-35%

- Under-35s: 18-22% of registered voters

- Under-35 turnout: 30-40%

- Under-35 share of actual votes: 8-12%

Any politician proposing to cut pensions loses 30-35% of votes. Any politician promising to protect pensions gains 30-35%.

The electoral incentive is clear: pander to retirees, fuck the young.

The Policy Outcomes:

During the 2010-2015 austerity period, European governments faced budget crises and had to cut spending. What got cut vs. what got protected reveals the political reality:

Cut heavily (youth programs):

- Education: -10 to -20% across most countries

- Youth employment programs: -30 to -50%

- University funding: -15 to -30%

- Housing support: largely eliminated

- Childcare subsidies: reduced or eliminated

Protected (elderly programs):

- Pensions: minimal cuts (3-8%), massive political resistance

- Healthcare: protected (disproportionately used by elderly)

- Subsidized transportation: pensioner discounts maintained

- Property tax breaks: maintained for retirees

- Winter fuel allowances: protected

The message: when money is tight, we cut the future to fund the past.

The Macron Example:

Emmanuel Macron's 2023 pension reform was the barest minimum:

- Raise retirement age from 62 to 64 (two years)

- Increase contribution period from 42 to 43 years (one year)

- No cuts to benefit levels

- Special regimes partially maintained

This tiny reform, retirement still lowest in developed world, triggered:

- Three months of continuous protests

- Garbage strikes (Paris buried in trash)

- Rail strikes (transport paralyzed)

- Refinery strikes (fuel shortages)

- Approval ratings collapsed

- Government nearly fell

Macron had to force it through using constitutional Article 49.3, bypassing a vote. Opposition parties filed no-confidence motions. The reform barely survived.

If raising the retirement age by two years causes this much political turmoil, what would real reform cost? Retirement at 70? Benefit cuts of 30%? Special regime elimination? It would trigger a revolution.

The Gerontocracy:

European leaders are all Boomers who will receive full pensions from the systems they're bankrupting:

- Ursula von der Leyen (EU Commission President): born 1958, gets full pension

- Emmanuel Macron (France): born 1977 (tail-end Boomer/early Gen X), gets full benefits

- Giorgia Meloni (Italy): born 1977, gets full benefits

- Olaf Scholz (Germany): born 1958, gets full pension

None of them will personally suffer from the pension crisis. Their children might, but they're insulated. The incentive to delay and deny is overwhelming.

The Millennial Political Weakness:

Why don't Millennials vote their interests? Multiple factors:

- Lower turnout (cynicism, pragmatism, less free time)

- Dispersed geographically (cities vs. countryside)

- Economically precarious (two jobs, no time for politics)

- Media controlled by Boomers (shapes narrative)

- Unions controlled by Boomers (protect their interests)

- Political parties led by Boomers (generational capture)

The entire political system is optimized for Boomer interests. Millennials can't vote their way out because the system is designed to prevent it.

"We do not inherit the earth from our ancestors; we borrow it from our children." - Native American Proverb

The Boomers didn't borrow. They took out a mortgage their children must pay, at interest rates the children can't afford.

WHAT THIS COSTS YOU

Your Pension Returns vs. Your Parents'

If you were born in 1950 (Boomer):

Worked: 1975-2020 (45 years)

Contribution rate: 10-12% of salary

Real wage growth during career: +100%

Total paid in: €180,000 (inflation-adjusted)

Retirement: age 62

Life expectancy: 85 (23 years retired)

Annual pension: €30,000

Total received: €690,000

Return on investment: 383%

If you were born in 1990 (Millennial):

Working: 2015-2060 (45 years)

Contribution rate: 24-33% of salary

Real wage growth during career: 0% (stagnant since 2000)

Total paying in: €360,000

Retirement: age 70 (if not raised further)

Life expectancy: 88 (18 years retired)

Projected annual pension: €18,000 (after 30-40% cuts)

Projected total received: €324,000

Return on investment: 90% (a 10% loss)

The extraction:

You pay: Double what your parents paid (€360k vs €180k)

You receive: Half what your parents receive (€324k vs €690k)

Your parents' gain: €510,000 more than they contributed

Your loss: €36,000 less than you contributed

That €510,000 your parents extracted? It came from you.

That's a house deposit they got, and you didn't.

That's your children's education they spent on themselves.

That's your retirement they consumed.

And they call you entitled.

The Impossible Budget

Your monthly income: €2,500 (average Millennial professional)

Required expenses:

- State pension contributions: €600 (24%)

- Rent/mortgage: €1,000 (40%)

- Utilities, food, transport: €500 (20%)

Subtotal: €2,100 (84% of income)

Remaining: €400 (16%)

What you're told to do with that €400:

- Private pension savings: €250/month minimum

(Inadequate, but necessary since state pension won't exist) - Emergency fund: €100/month

(Need 6 months expenses = €15,000, will take 12+ years) - House deposit savings: €50/month

(Need €50,000 for 10% deposit, will take 83 years)

Total required: €400

Remaining: €0

What this budget doesn't include:

- Healthcare costs

- Dental care

- Childcare (if you have kids)

- Children's education

- Car repairs

- Clothing

- Entertainment

- Vacations

- Gifts

- Emergencies

- Life

This is why Millennials:

- Aren't buying houses (can't save deposits)

- Aren't having children (can't afford them)

- Aren't saving for retirement (money doesn't exist)

- Are living with parents into 30s (only way to survive)

- Are delaying everything (waiting for financial stability that never comes)

It's not avocado toast. It's mathematics.

You cannot pay 24% for pensions you won't receive, 40% for housing that Boomers made unaffordable, and still have enough left for a life.

The system is designed to extract everything from you while telling you you're not working hard enough.

The Inheritance Trap

Boomers to Millennials: "You'll inherit our wealth eventually."

The reality:

When Boomers die:

- Average age at death: 88

- Children's age when inheriting: 63

You'll inherit wealth you needed at:

- Age 25: University (parents said "pay it yourself," average €40,000 debt)

- Age 30: House deposit (need €50,000, couldn't save it)

- Age 35: Starting family (childcare €1,500/month, couldn't afford)

- Age 40: Children's education (€30,000 per child, went into debt)

- Age 50: Caring for aging parents (€2,000/month care costs, impoverished you)

But you receive it at: Age 63

(When you're retiring with nothing because pension system collapsed)

What reduces the inheritance:

- Care home costs: €60,000-€100,000 per parent (4-5 years average)

- Medical expenses: €20,000-€40,000 (final years)

- Funeral costs: €5,000-€10,000

- Probate fees: 3-5% of estate

- Inheritance tax: 40% on amounts over threshold

- Sibling splits: Divided 2-4 ways typically

- Property value at death: Often mortgaged for care costs

What you actually inherit:

- Cash after costs: €30,000-€60,000 per child

- Property: Often sold for care, or so outdated needs €50,000+ renovation

- Timing: 1-2 years after death (probate delays)

- Age when received: 63

What you could have done with that money at 30:

- House deposit: €50,000 = house ownership

- Compound interest 33 years at 5%: €50,000 becomes €240,000

- Avoided rent payments: €1,000/month × 33 years × 12 = €396,000 saved

- Wealth building: Own asset, build equity, financial security

What you'll do with it at 63:

- Supplement pension that doesn't exist

- Pay off debts accumulated over lifetime

- Afford basic retirement

- Too late to compound

- Too late to build wealth

- Too late to help

The extraction mechanism:

Boomers locked their wealth in housing (up 400% in value)

Told you to "save and inherit"

Needed their wealth during your prime earning years

Received it after your life was set

Inheritance taxed heavily

Reduced by care costs

Arrives too late to matter

This isn't a wealth transfer. It's wealth locked away until it's useless, then taxed when released.

The Private Pension Scam

Millennials are told: "The state pension won't be enough, you need to save privately." True. But the private pension industry is a fee extraction racket that ensures you can't.

The Fee Structure:

UK example (one of the "better" systems):

Contributions: €100/month for 40 years

- Total contributed: €48,000

- Expected growth at 5% annually: €150,000

- Actual value after fees: €95,000

- Total fees extracted: €55,000 (37% of returns)

Fee breakdown:

- Annual management fee: 0.75% (sounds small, compounds brutally)

- Platform fee: 0.25%

- Fund fees: 0.3-0.5%

- Entry charges: 5% of contributions

- Exit charges: possible

- Performance fees: 20% of gains above benchmark

That 0.75% annual fee? Over 40 years it eats 30-35% of your pot. Add the other fees and you're losing 35-40% of returns to fund managers.

Frequently Asked Questions

Q: Didn't boomers pay into the system their whole lives? Don't they deserve their pensions?

A: Yes, Boomers paid in, but at much lower rates (10-15% vs 20-33% today), for fewer years (often 35 vs 43+ required now), during economic boom times (wages doubled during their careers vs stagnant since 2000). And they're taking out far more than they paid in. The average French boomer paid in €180,000 and will receive €685,000, a 380% return. That's not "what they paid for", it's extraction from current workers. Millennials will pay in €360,000 and receive maybe €180,000 if lucky. The "I paid in" defense ignores that Boomers paid in far less than they're taking out, and someone has to cover the difference. That someone is their children.

Q: Isn't this just how pension systems work, young pay for old, then their children pay for them?

A: Pay-as-you-go systems only work when demographics are stable and benefits are modest. Boomers benefited from favorable demographics: 5 workers per pensioner when they were working. Millennials face 1.5 workers per pensioner when they retire, the system cannot support them. Boomers also voted to expand benefits (increasing payments by 40% in real terms) while refusing to increase funding proportionally. The generational compact was supposed to be reciprocal, you pay for your parents, your children pay for you at similar rates. Boomers broke it by taking far more than they paid in and leaving a bankrupt system.

Q: Can't we just raise taxes to keep pensions funded?

A: We already tried. Pension contributions rose from 10-15% to 20-33% of salary. To maintain current Boomer pension promises would require increasing to 40-50% by 2040, plus income tax, plus consumption tax. Total tax rates would hit 70-80%, which would destroy economic activity and trigger political revolution. You cannot tax your way out of demographic mathematics. When you have 1.5 workers per pensioner instead of 5, the math simply doesn't work at any tax rate.

Q: What about private pensions, aren't they the solution?

A: Private pensions would help if workers could afford them. But Millennials already pay 20-33% of salary to fund Boomer state pensions, leaving little for private savings on stagnant wages with housing costs at 40-50% of income. Plus, private pensions have massive problems: fees eat 30-40% of returns over 40 years, market crashes destroy wealth (2022: many funds cut benefits 20%), and longevity risk means you might outlive your savings.

Q: Didn't boomers build the system and work hard, haven't they earned these benefits?

A: Boomers voted for benefit expansions in the 1970s-1990s while cutting their own taxes and refusing adequate funding increases. They expanded their own benefits knowing their children would pay for them. They voted themselves early retirement, index-linked increases, special regimes, and generous terms, then refused to fund any of it sustainably. This isn't a system they built through hard work, it's a Ponzi scheme that worked only while demographics favored them.

Q: Why not just cut pensions to sustainable levels instead of burdening the young?

A: Politically impossible. Pensioners are 25-30% of voters with 75%+ turnout = 30-35% of actual votes. Youth are 18-22% of voters with 30-40% turnout = 8-12% of votes. Any politician proposing meaningful pension cuts loses 30-35% of votes and the next election. Emmanuel Macron tried raising France's retirement age from 62 to 64, two years, and faced months of riots, government paralysis, and near-collapse.

Q: Isn't the real problem immigration, not pensions?

A: Immigration could help demographics but can't solve the pension crisis. To restore 1970s worker-to-pensioner ratios (5:1) would require 100+ million immigrants across the EU, economically disruptive, socially impossible, politically toxic. Plus immigrants age too, they eventually become pensioners themselves, just delaying the problem. The real problems are benefit levels that are too high, retirement ages that are too low, and a generation that refuses to accept reality.

Q: What about means-testing pensions, only pay them to people who actually need the money?

A: Means-testing is a sensible solution that Boomers categorically refuse. Wealthy pensioners sitting on €500,000+ in housing wealth still collect full state pensions funded by workers earning €30,000. Means-testing would save €50-€70 billion annually across the EU by not paying pensions to millionaires. But politically: "I paid in, I deserve it" (ignoring they paid in far less than they're taking out).

Q: Can't economic growth solve this?

A: Not unless growth returns to 1950s-1970s levels, which is impossible. Post-2008 growth averages 1-2% annually. Pension promises assume 3-4% growth. That gap is structural, productivity gains flow to capital not labor (wages stagnant for 20 years), automation replaces workers (fewer contributors), and birth rates ensure shrinking workforce.

Q: Aren't younger generations just entitled and lazy?

A: Millennials are the most educated generation in history, work longer hours (especially counting gig economy), and face higher costs of living than any generation since WWII. They pay 20-33% of salary into pensions (Boomers paid 10-15%), can't afford housing that Boomers bought at 3x income (now 10x income), have precarious employment instead of jobs for life. Calling them lazy while extracting their income for your €30,000/year pension is boomer gaslighting.

Q: What actually happens when these pension systems collapse?

A: Three scenarios, all bad. Scenario 1: Slow squeeze, benefits gradually cut, retirement age incrementally raised, permanent austerity for workers. Scenario 2: Sudden default, governments announce immediate 30-50% pension cuts like Greece 2010-2015, riots and political crisis ensue. Scenario 3: Hyperinflation bailout, governments print money to pay pension promises, currency collapses, inflation destroys real value of pensions, both young and old impoverished.

Q: Is there ANY way forward that doesn't completely screw younger generations?

A: Yes, but it requires political courage that doesn't exist. Honest reforms now: (1) Means-test state pensions, (2) Raise retirement age to 70+, (3) Index pensions to inflation not wages, (4) Eliminate special regimes, (5) Wealth tax on Boomer assets, (6) Shift to funded individual accounts for younger workers. They're politically toxic because Boomers vote at 75% and would reject any politician proposing them.

What Needs to Change

Immediate Reforms:

- Means-Test State Pensions - No pension if assets above €500,000. Saves €50-€70B annually.

- Equalize Retirement Ages - Everyone retires at 70, no special regimes. Saves €80-€100B annually.

- Index Pensions to Inflation Only - Stop relative gains to workers. Saves €30-€40B annually.

- Remove Upper-Income Tax Advantages - Wealthy don't need pension tax incentives. Saves €20-€30B annually.

- Intergenerational Wealth Transfer Tax - One-time wealth tax on estates above €1M. Raises €100B+.

Structural Transformation:

- Shift to funded individual accounts where workers save for themselves

- End pay-as-you-go Ponzi structure

- Create Intergenerational Fairness Commission to block unfair policies

Why None of This Will Happen:

Pensioners are 30-35% of actual voters. Youth are 8-12%. Electoral math makes reform impossible until crisis forces it. Europe will delay until demographics make the system impossible, then brutal cuts will be imposed.

Conclusion: The Theft Continues

The European pension system is the largest peacetime wealth transfer in history. Trillions of euros have flowed from young workers to old retirees through a mechanism designed to look like a social contract but functioning as organized extraction.

The numbers are undeniable:

- Italy: 16.2% of GDP on pensions, mathematically unsustainable

- France: 383% return for Boomers, 90% loss for Millennials

- Greece: system collapsed, pensioners lost 40-50%

- Spain: reserve fund raided, €67B to €2B in 13 years

- Germany: demographic time bomb, reform paralyzed

The mechanics are transparent:

- Boomers paid in €180,000, taking out €685,000

- Millennials paying in €360,000, will receive €180,000 if lucky

- Difference: €505,000 extracted per Boomer, paid by their children

The political capture is complete:

- Pensioners: 30-35% of votes

- Youth: 8-12% of votes

- Reform: electoral suicide

- Collapse: inevitable

The moral obscenity is staggering. Boomers benefited from unprecedented prosperity, bought houses at 3x income, got jobs for life with pensions, voted themselves generous benefits, refused to fund them adequately, left children with debt and broken promises, then called them lazy.

And through it all, the extraction continues. Every month, Millennials pay 20-33% of their salary into systems that will give them 30-50% less than they paid in, while Boomers collect benefits four times what they contributed.

This isn't a pension crisis. It's an intergenerational theft so massive it makes every other European scandal look trivial.

And the theft continues because the thieves vote, and the victims don't.

"It is not the young people that degenerate; they are not spoiled till those of mature age are already sunk into corruption." - Montesquieu

The corruption is boomer extraction disguised as entitlement.

No ads. No sponsors. Just signals from the noise.

Keep The Kade Frequency transmitting.

The Kade Frequency is independent investigative journalism on institutional corruption and power. No corporate sponsors. No EU funding. No ads. Just truth.